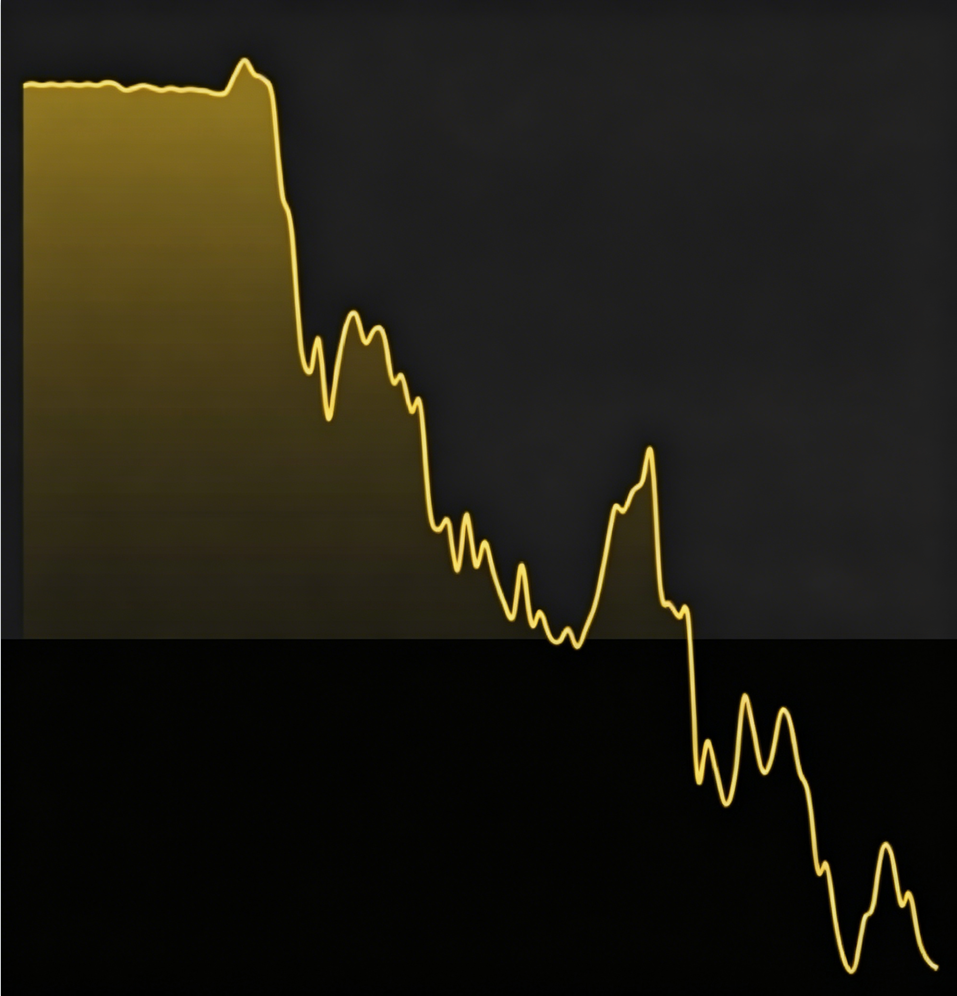

Gold prices suffered a sharp sell-off on June 10th, 2026, falling through the key $4,200 per ounce level for the first time since March 23rd and hitting a near three-month low as a stronger U.S. dollar and rising Treasury yields weighed heavily on the precious metal. Spot gold dropped as much as 1.9 percent intraday to around $4,181 an ounce, breaching the crucial psychological support level, before recovering slightly. The slide extended losses that began on June 5th, when gold suffered its steepest single-day decline in months, falling 3.25 percent following an unexpectedly strong U.S. jobs report. From its record high of nearly $5,600 per ounce reached in late January, gold has now fallen more than 20 percent, placing it firmly in technical bear market territory. Major gold mining stocks listed in Hong Kong tumbled in tandem, with Chifeng Gold dropping over 7 percent and other sector heavyweights falling more than 3 percent on the day. In China’s retail market, the sharp decline in international prices was quickly transmitted to the consumer level, with major jewelry brands cutting their gold product prices below the 1,300 yuan per gram threshold.

The breakdown in gold prices has been driven by a fundamental shift in market expectations surrounding U.S. monetary policy. The catalyst came on June 5th, when the U.S. Labor Department reported that non-farm payrolls had increased by 172,000 jobs in May, more than double the market consensus forecast of 85,000, while prior months’ figures were also revised higher. The stronger-than-expected data dramatically revised market pricing for Federal Reserve policy. By June 9th, Fed Watch data showed that the market attached a probability of around 70 percent for at least one interest rate hike by December 2026, the first such pricing since the market had previously bet on rate cuts for the year. Higher benchmark rates increase the opportunity cost of holding non-interest-bearing assets like gold, prompting large institutional investors to unwind bullish positions. The resulting jump in Treasury yields – with the 10-year note surpassing 4.5 percent and the 30-year bond breaking above 5 percent – has further eroded gold‘s appeal as an alternative asset. The U.S. dollar index has also moved decisively higher, gaining ground above the 99 level and at times touching 100, making dollar-priced gold more expensive for holders of other currencies.

Global gold exchange-traded funds have registered persistent outflows as investors flee the metal. According to the World Gold Council, global physically-backed gold ETFs saw net outflows of approximately $2 billion in May 2026, ending five consecutive months of inflows. Total assets under management in these products fell about 2 percent to $604 billion in May, with holdings modestly declining to 4,121 metric tons, slightly below the all-time high of 4,176 tons reached in late February. In China, the largest gold ETF saw its assets shrink from a peak of more than 130 billion yuan to below 100 billion yuan amid the steep sell-off. According to analysts, the evaporation of paper gold demand stems from a combination of interest rate risks, profit-taking after a record rally in 2025, and reduced retail investor enthusiasm as prices have fallen almost continuously for several weeks.

While the near-term outlook for gold remains clouded by the prospect of tighter U.S. monetary policy, institutional views on the longer term remain sharply divided. Among the bears, Citigroup has lowered its three-month gold price target to $4,000 an ounce from $4,300, and warned that if the Strait of Hormuz remains closed into late summer, weakening physical demand could drive prices as low as $3,500 an ounce. On the other hand, banks including Goldman Sachs, Bank of America and Morgan Stanley have maintained constructive long-term forecasts, citing structural factors such as sustained central-bank accumulation, ongoing reserve diversification away from the U.S. dollar and eventual Federal Reserve rate cuts expected later in the cycle. Notably, central banks have continued to add to their gold reserves even as prices have fallen. The People’s Bank of China raised its gold holdings for the 19th consecutive month in May 2026, adding an additional 320,000 ounces, while Poland, the Czech Republic and other central banks in Eastern Europe and Asia have also remained active buyers. Until the Federal Reserve’s policy path becomes clearer, however, gold prices seem likely to face continued selling pressure. The next major test for the metal will be the U.S. Consumer Price Index reading for May and the Federal Reserve’s June policy meeting, either of which could provide fresh direction for the volatile market.